Class 11 Accountancy Chapter 1 Summary Notes PDF Download

Vedantu provides complete Introduction to Accounting Class 11 Notes in FREE PDF format. This chapter lays the foundation for understanding the basic principles and concepts of accounting. It covers essential topics such as the meaning, objectives, and importance of accounting, which are crucial for students beginning their journey in commerce. These Class 11 Accountancy Notes are designed to simplify key concepts and help students prepare effectively for their exams, ensuring a solid grasp of the fundamentals, and ultimately the Class 11 Accountancy Syllabus.

Table of Content

Table of ContentAccounting

Accounting is an art of recording, classifying and summarizing the monetary transactions in an efficient manner and interpreting the results.

Functions of Accounting

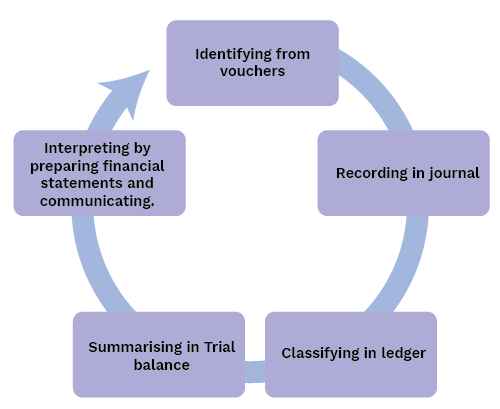

Identifying: Identifying the business transactions from various sources is the first step of accounting.it involves observing all business activities and identifying those which are considered as financial transactions.

Recording: Only those transactions are recorded in books of accounts which can be measured in terms of money. It involves recording them in a journal and keeping a systematic record of all of them.

Classifying: After recording the transactions they are classified. Classification refers to the grouping of all the transactions of same nature at one place.

Summarising: It is the process of putting the balances of all accounts at one place i.e. Trial balance.

Communicating: Accounting also includes the communication of financial data like financial statements to the users who analyse them as per individual requirements.

Objectives of Accounting

To maintain proper records of business transactions according to specified rules which helps them to minimize the chance of omission and fraud.

To ascertain the net profit or loss suffered on account of business transactions during a particular period and to know the exact reasons leading to profit or loss.

To ascertain the financial position of business by means of financial statement i.e,Balance sheet.

To ascertain the progress of business from year to year and to detect errors and frauds.

To provide accounting information to various interested parties like owners, creditors, banks, employees etc. who perform an in depth analysis as per the requirement of the stakeholders.

Advantages vs Limitations of Accounting:

Here's the information presented in a table format:

Book-Keeping-Base of Accounting

Book keeping is an art of recording the transactions in the books of accounts. Only those transactions which bear a monetary value are recorded. It is the first step of accounting. Its main purpose is record keeping or maintenance of books of accounts, It should not be confused with accounting. Differences between the two are as follows.

Subfields of Accounting

Financial Accounting:The main purpose of this branch is to record the business transactions in a systematic manner, to ascertain profit or loss and to present the financial position of the business with the help of a balance sheet.

Cost Accounting: The main purpose of cost accounting is to ascertain the total cost and per unit cost of goods produced and services rendered by business.

Management Accounting: The main purpose of this branch is to present the accounting information in such a way as to assist the management in planning and controlling the operations of business.

Tax Accounting: This branch is used for tax purposes. Income tax and gst are computed on the basis of this accounting.

Qualitative Characteristics of Accounting Information

Accounting information should be prepared and presented in such a way that is able to depict a clear view of business enterprise.

1. Reliability: It implies that information must be factual and verifiable. And free from errors.

2. Relevance: Accounting information must be relevant to the objectives of enterprise. To be relevant, information must help the users of accounting information in making decisions.

3.Understandability: Accounting information should be presented in such a manner that they are understood easily by their users such as investors, employees, etc.

4. Comparability: It is a very useful quality of accounting information. Financial statements should contain previous year data so that it can be compared with current year so that current performance be compared with past performance.

Accounting Terms

Business Transaction: A Business transaction is an economic activity of business that changes its financial position.

Account: It is a record of all business transactions relating to a particular person or item. It is a T Shaped proforma.

Capital: It refers to the amount invested by the owner in a business. The amount invested could be in the form of cash, goods, etc.

Drawing: Any cash or goods withdrawn by the owner for personal use made out of business funds are known as drawings.

Profit: It is the excess of total revenue over total expense of a business. Profit =Revenue-Expenses.

Loss: The excess of expenses over related revenue is known as loss. Loss= Expenses-Revenue.

Gain: It is a monetary benefit resulting from events or transactions which are incidental to business like profit on sale of fixed assets.

Stock: It includes goods unsold on a particular date.

Purchases: It refers to the amount of goods bought by business for resale or use in production.it can be of cash or credit.

Purchase return: When purchased goods are returned to suppliers, it is referred to as purchase return.

Sales: It means transfer of goods or services for money in the normal course of business.

Sales return: When customers return the goods sold to them it is known as sales returns.

Debtors: It refers to those persons whose business has been sold goods on credit and payment has not been received yet.

Creditors:It refers to those persons whose business buys goods on credit and payment has not been done yet.

Voucher: A voucher is a written document which is created in support of a particular transaction. It may be in the form of a cash memo, invoice or receipt. Voucher is a necessary component of auditing.

Income: It is the difference between revenue and expense.

Expense: It is the amount used in order to produce and sell goods and services.

Discount: It is the rebate given by the seller to the buyer. It is of 2 types: Cash Discount and Trade Discount.

Cash Discount: When discount is allowed to customers for making prompt payment.It is always recorded in books of accounts.

Trade Discount: This is a type of discount allowed by the sellers to their customers at a fixed percentage on the list price of goods. and also it is not entered in the books of accounts.

Bad Debts: It refers to the amount that debtor has not paid even after repeated reminders and has no intention of paying in the future.

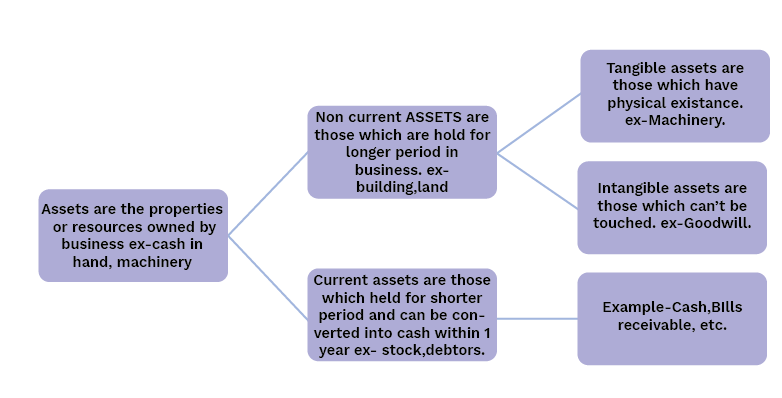

Assets

Liabilities

Liabilities refers to financial obligations of business.it denote the amount which a business owes to others.ex- Creditors,loan,etc.It is of 2 types;

Non current liabilities: It refers to those which fall due for payment in a relatively longer period. For ex- long term loans.

Current liabilities: It refers to those which are to be paid in the near future. Ex-Creditors, Outstanding expenses.

Expenditure

It involves spending cash or incurring a liability for the purpose of acquiring assets,goods or services. It is of 3 types.

Revenue Expenditure: It refers to any expenditure,the full benefit of which is received during one accounting period.ex-salaries,rent.

Capital Expenditure: It refers to expenditure,the benefit of which is received during more than one year. Ex- Machinery.

Deferred Revenue Expenditure: It refers to expenditure which are revenue in nature but benefit of which is likely to be derived over no of years. Example-Advertisement.

5 Important Topics of Class 11 Accountancy Chapter 1 you shouldn’t Miss

Importance of Class 11 Accountancy Chapter 1 Notes

The Class 11 Accountancy Chapter 1 Notes simplify complex accounting concepts for easier understanding and retention.

The Class 11 Accountancy Chapter 1 Notes PDF provide a structured overview of essential topics like objectives, importance, and principles of accounting.

These notes facilitate quick revision and reinforcement of key ideas, crucial for exam preparation.

The Accountancy Class 11 Chapter 1 Notes help students save time by offering concise and clear explanations.

These notes enhance practical understanding, laying a strong foundation for future studies in commerce.

The Class 11 Accountancy Chapter 1 Notes PDF is available for FREE download from the Vedantu website enabling offline access anywhere anytime as you want.

The Notes of Accountancy Class 11 Chapter 1 are provided by top subject matter experts at Vedantu, thus ensuring complete accuracy and relevance of the content provided.

Tips for Learning Chapter 1 Introduction to Accounting Class 11 Notes

Begin by reading through Vedantu’s Introduction to Accounting Class 11 notes to understand the fundamental concepts, such as the meaning and objectives of accounting. This will give you a strong foundation.

While studying, highlight or underline important terms and definitions in the notes. This will help in quick revision before exams.

Pay special attention to the examples provided in the notes. They help in understanding how theoretical concepts are applied in real-life scenarios.

Schedule regular revision sessions with Vedantu’s notes to reinforce your understanding. Frequent revision helps in retaining information longer.

Compare the concepts in the current chapter with related topics in future chapters using Vedantu's Class 11 Accountancy Chapter 1 Notes PDF. This will help you see the connections and deepen your understanding.

If you come across any doubts or unclear concepts, revisit the specific section in Vedantu's notes or seek help from Vedantu's online resources.

Conclusion

Class 11 Accountancy Chapter 1, Introduction to Accounting, provides a fundamental understanding of accounting principles, laying the groundwork for more advanced topics in commerce. This chapter covers essential concepts like the objectives, importance, and basic principles of accounting, which are crucial for any student pursuing commerce. Vedantu's revision notes for this chapter offer a clear and concise explanation of these topics, making it easier for students to grasp the material. These notes are an invaluable resource for exam preparation, helping students to review key points quickly and efficiently. By using Vedantu's notes, students can solidify their understanding and be well-prepared for their exams.

Related Study Materials for Class 11 Accountancy Chapter 1

Chapter-wise Revision Notes Links for Class 11 Accountancy

Important Study Materials for Class 11 Accountancy

FAQs on Introduction to Accounting Class 11 Accountancy Chapter 1 CBSE Notes - 2026-27

1. What is the core concept of accounting that I should remember for a quick revision?

For a quick recap, remember that accounting is a systematic process of identifying, recording, classifying, summarising, interpreting, and communicating financial information. Its main purpose is to provide clear and useful data about a business's financial performance and position to various stakeholders.

2. What are the primary objectives of accounting in Chapter 1?

The primary objectives of accounting, as covered in the introductory chapter, are to:

- Maintain a systematic record of all business transactions.

- Calculate the net profit or loss for a specific period.

- Determine the financial position of the business through the Balance Sheet.

- Provide essential financial information to various users like owners, managers, and creditors for decision-making.

3. How is book-keeping different from accounting, and why is this distinction important for understanding the subject?

The key difference is that book-keeping is just the recording phase of accounting—it's about correctly entering financial transactions in the books. Accounting is a much broader concept that includes not only recording but also summarising, analysing, and interpreting that data to generate insights. This distinction is crucial because book-keeping provides the raw data, while accounting turns that data into meaningful information for strategic decisions.

4. What are the key qualitative characteristics that make accounting information useful?

To be useful, accounting information must possess four key characteristics:

- Reliability: The information must be factual, verifiable, and free from error or bias.

- Relevance: The information must be capable of influencing the decisions of its users.

- Understandability: It must be presented in a clear and concise manner so that users can easily comprehend it.

- Comparability: The information should allow users to compare a firm's performance over time and against other firms.

5. Why is accounting often called the 'language of business'?

Accounting is called the 'language of business' because it communicates the financial results and health of an organisation to various stakeholders. Just as a language uses words to convey ideas, accounting uses financial statements like the Profit & Loss Account and Balance Sheet to report on a company's activities and performance, enabling informed business decisions.

6. What is the fundamental difference between an 'asset' and a 'liability'?

An asset is an economic resource owned by a business that is expected to provide future benefits (e.g., cash, machinery, stock). In contrast, a liability is a financial obligation or debt that the business owes to another party (e.g., loans from a bank, amounts owed to suppliers). Simply put, assets are what a business owns, and liabilities are what it owes.

7. Can you explain the difference between 'Capital' and 'Drawings'?

Capital is the amount invested in the business by its owner(s), which can be in the form of cash or assets. It represents the owner's claim on the business's assets. Drawings, on the other hand, refer to any cash or goods withdrawn from the business by the owner for personal use. Capital increases the owner's equity, while drawings decrease it.

8. How does the distinction between Capital Expenditure and Revenue Expenditure affect the summary of a company's finances?

This distinction is crucial for accurate financial reporting. Capital Expenditure is an amount spent to acquire a long-term asset (like machinery) and is shown on the Balance Sheet. Its benefit lasts for more than one year. Revenue Expenditure is an expense incurred for day-to-day operations (like salaries) and is shown in the Trading and Profit & Loss Account. Incorrectly classifying these can distort the reported profit and the company's financial position.

9. Who are the main users of accounting information according to the CBSE syllabus?

The users of accounting information are broadly classified into two groups:

- Internal Users: These are individuals within the organisation, such as owners and management, who use the information for planning, controlling, and decision-making.

- External Users: These are individuals or entities outside the organisation, including investors, creditors, banks, and government authorities, who use the information to assess the business's profitability and financial soundness.

10. Why does accounting only record transactions that can be measured in money? What is the main drawback of this principle?

Accounting uses money as a common denominator to record and compare diverse business activities, a concept known as the Money Measurement Principle. This allows for uniform and objective financial reporting. The major drawback is that it ignores crucial non-monetary factors that significantly impact a business, such as the skill of the management team, employee morale, or brand reputation, as these cannot be assigned a precise monetary value.